EWallet App Development

In House VS Outsourced eWallet Development: Which Is Better for US Startups?

January 20, 2026

January 20, 2026

The digital payments ecosystem in the United States is evolving rapidly, making eWallet applications a core component of modern fintech innovation.

From mobile payments and peer-to-peer transfers to loyalty programs and crypto integrations, eWallets are transforming how consumers and businesses handle transactions.

For US startups entering this competitive landscape, building a secure, scalable, and regulation-compliant eWallet app is both an opportunity and a challenge.

This guide provides a detailed, experience-backed comparison to help US startups make an informed, strategic decision aligned with their growth goals.

In-house eWallet app development process involves building the application using an internal team of developers, designers, quality analysts, and product managers employed directly by the startup.

For US startups with strong technical leadership and sufficient funding, in-house development offers direct oversight and deep alignment with business objectives.

Teams can iterate quickly on feedback, maintain strict control over sensitive financial data, and build proprietary intellectual property over time.

This model is often favored by startups planning long-term product expansion or multiple fintech offerings.

|

Pros |

Cons |

|

Full control over code and roadmap |

High hiring and operational costs |

|

Strong internal security oversight |

Longer development timelines |

|

Direct team collaboration |

Limited flexibility in scaling |

|

Complete IP ownership |

Ongoing HR and compliance burden |

Outsourced eWallet app development involves partnering with multiple third-party top eWallet app development companies that specialize in fintech solutions.

The external team handles design, development, testing, compliance implementation, and occasionally post-launch support, as per the agreed-upon scope.

Experienced development partners bring pre-built frameworks, proven security practices, and in-depth knowledge of financial regulations, including PCI DSS, KYC, and AML.

Outsourcing also allows founders to focus on fundraising, partnerships, and customer acquisition rather than technical execution.

|

Pros |

Cons |

|

Lower upfront and operational costs |

Reduced direct control |

|

Faster time-to-market |

Time zone and communication gaps |

|

Access to fintech specialists |

Dependency on external teams |

|

Easy team scalability |

Requires strong data protection agreements |

For most startups, total development expenses fall between $20,000 and $120,000, depending on the chosen model.

The following are the differentiations of the two models in terms of the eWallet app development cost incurred for developing them.

In-house eWallet app development involves building a dedicated internal team and maintaining the required technical infrastructure.

For US startups, assembling a lean in-house team consisting of mobile developers, backend engineers, UI/UX designers, and QA specialists can result in initial development costs ranging from $60,000 to $120,000 for a basic to moderately complex eWallet application.

These costs include salaries, onboarding, development tools, cloud infrastructure, and internal testing resources.

Estimated Cost Range (In-House): $60,000–$120,000

Outsourced development offers a more cost-efficient and predictable pricing structure, making it a preferred choice for many US startups.

The cost of outsourcing an eWallet app typically ranges from $20,000 to $70,000, depending on features such as user authentication, payment gateway integration, transaction history, admin dashboards, and compliance implementation.

Outsourcing allows startups to launch MVPs faster while maintaining budget control. It also enables easy scaling and optional post-launch support without long-term financial commitments.

Estimated cost to build an eWallet app (outsourced): $20,000–$70,000

The following is the table that differentiates the cost of both in terms of their features.

|

Cost Parameter |

In-House eWallet Development |

Outsourced eWallet Development |

|

Estimated Total Cost |

$60,000–$120,000 |

$20,000–$70,000 |

|

Initial Setup & Onboarding |

High (recruitment, training, internal setup) |

Low (ready-to-deploy development teams) |

|

Team Structure |

Full-time developers, designers, QA, DevOps |

Dedicated or shared fintech experts |

|

Development Timeline |

Longer due to hiring and setup |

Faster with proven frameworks |

|

Infrastructure & Tools |

Self-managed servers, licenses, and security tools |

Included in project cost |

|

Compliance Implementation (PCI DSS, KYC, AML) |

Requires internal expertise and audits |

Built-in fintech compliance experience |

|

Maintenance & Updates |

Ongoing internal operational expense |

Optional, contract-based support |

|

Best Suited For |

Well-funded, growth-stage startups |

Early-stage and MVP-focused startups |

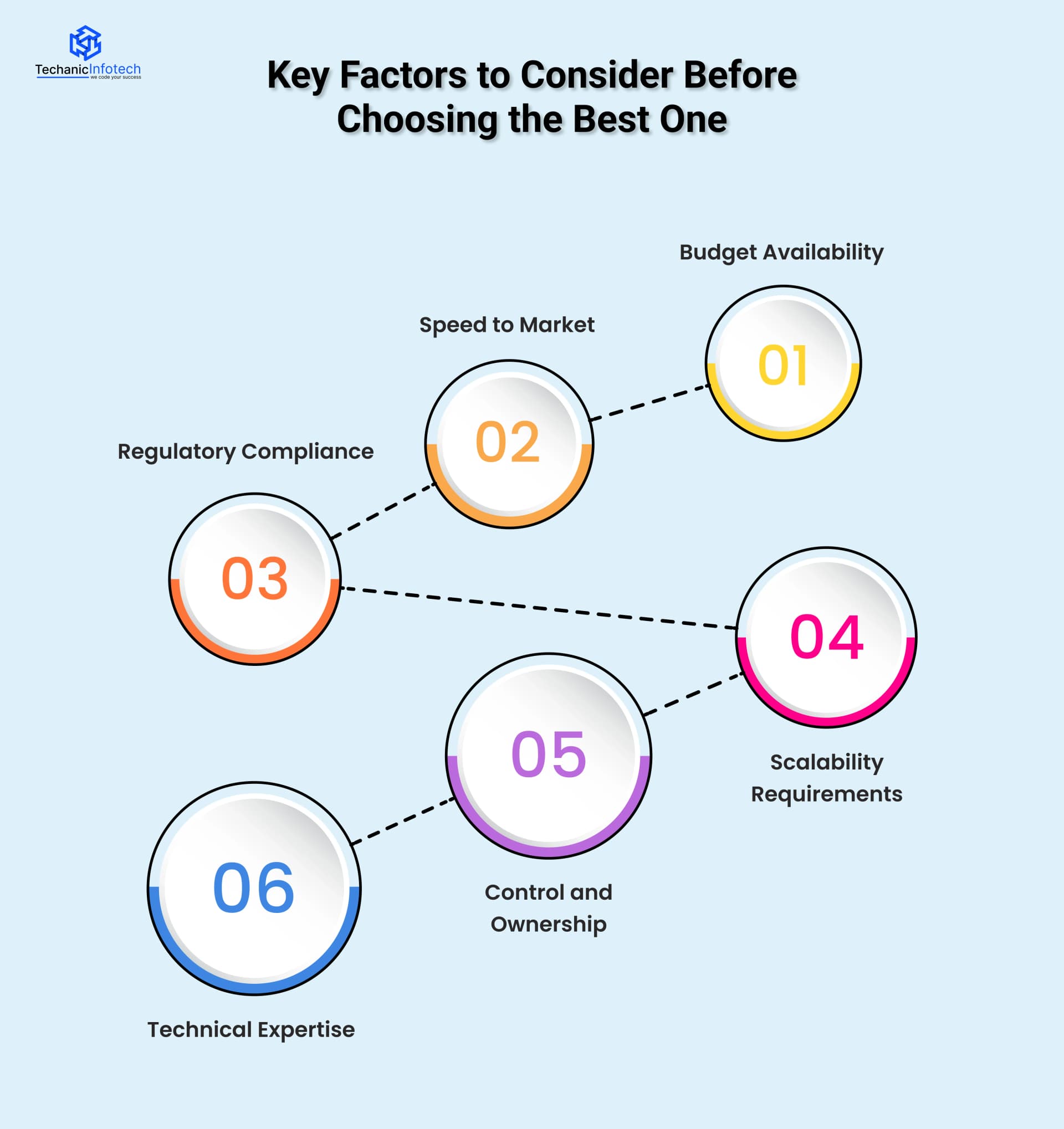

Choosing the right eWallet app development model requires careful evaluation of eWallet app development timeline, financial capacity, compliance needs, scalability goals, and technical expertise to ensure long-term success for US startups.

The following are the key factors that one should consider when choosing the best one.

Budget constraints significantly influence the development model a startup can sustain.

Early-stage startups with limited capital often benefit from outsourcing due to lower upfront costs and predictable pricing.

In contrast, well-funded startups may afford in-house teams, absorbing long-term expenses such as salaries, infrastructure, compliance audits, and continuous upgrades without financial strain.

Time-to-market is critical in the competitive fintech ecosystem with best marketing strategy of eWallet app.

Outsourced development teams leverage pre-built fintech frameworks, established workflows, and agile methodologies to accelerate MVP launches.

In-house teams may face delays caused by recruitment, onboarding, and internal process setup, which can slow product validation and early user acquisition.

eWallet applications must comply with strict US financial regulations, including PCI DSS, KYC, and AML requirements.

Outsourcing partners with proven fintech experience often have compliance-ready architectures and standardized security practices.

This reduces regulatory risks, minimizes errors, and ensures smoother audits compared to startups managing compliance internally for the first time.

Startups must anticipate future growth when choosing a development model.

Outsourced teams offer rapid scalability by adding or reducing resources as needed, without long-term commitments.

In-house scaling requires hiring additional staff, increasing infrastructure, and expanding operational budgets, which can be costly and time-consuming during high-growth phases.

In-house development provides direct control over the development roadmap, codebase, and security protocols.

However, outsourcing does not mean losing ownership. With clear contracts, NDAs, and intellectual property clauses, startups can retain full IP rights while benefiting from external expertise and faster development cycles.

Building a secure and scalable eWallet app requires specialized fintech knowledge.

Startups without prior experience in payment systems, encryption, or compliance benefit significantly from outsourcing to experts.

Experienced fintech partners reduce technical debt, improve architecture decisions, and ensure best practices are followed from the initial development stage.

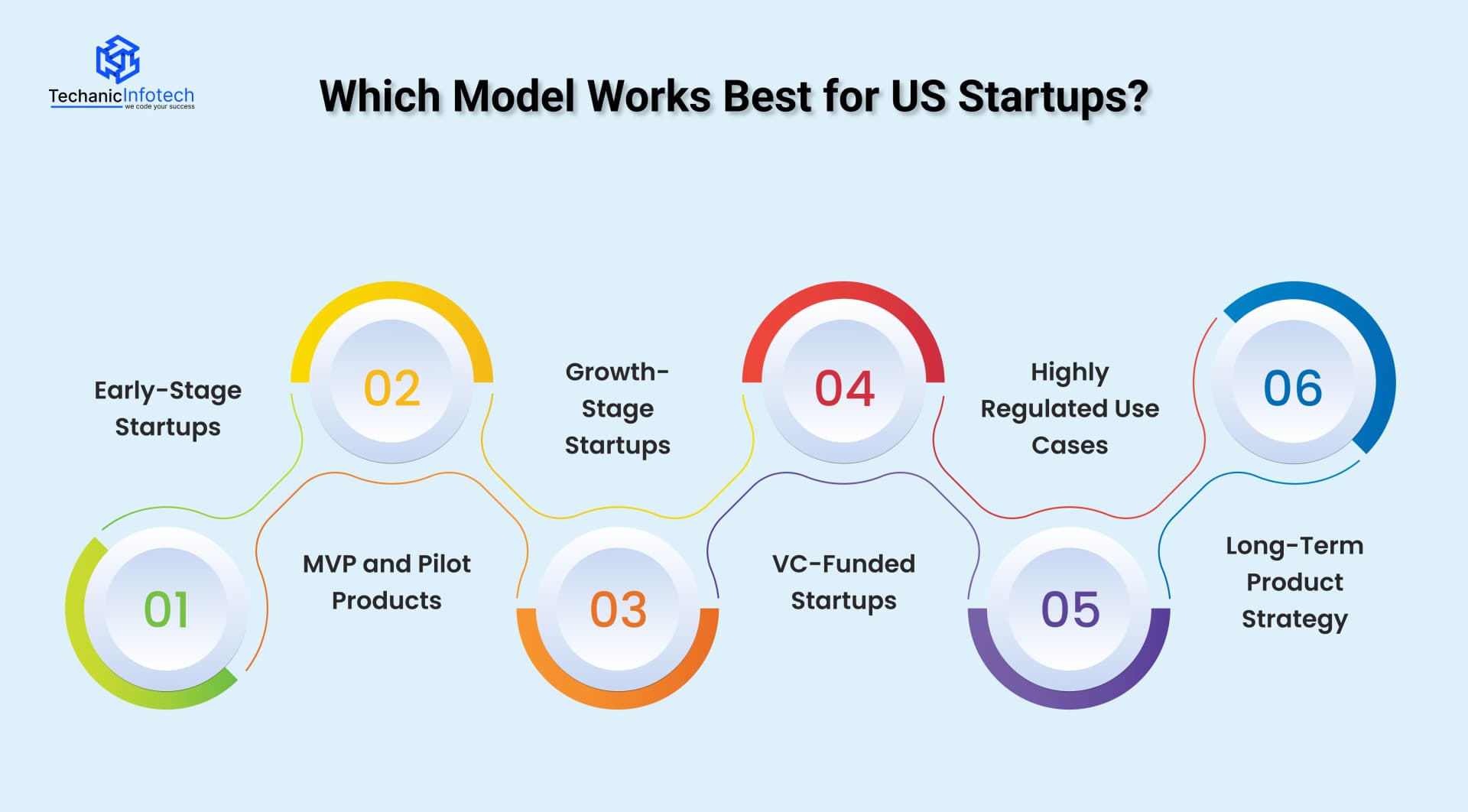

Choosing the right eWallet app development business model depends on a startup’s stage, funding, regulatory exposure, and long-term vision, as different growth phases demand different one.

For early-stage startups, outsourcing is often the most practical choice. It allows founders to validate their business idea quickly without heavy upfront investment.

Outsourcing reduces financial risk, speeds up development, and provides access to experienced fintech professionals who can guide product decisions during the critical validation phase.

Example:

A US-based fintech startup validating a peer-to-peer payment concept outsourced its MVP development to a fintech partner.

The product launched in under four months, helping the founders secure seed funding based on early user traction.

When building an MVP or pilot version of an eWallet app, speed and flexibility are essential.

Outsourced development teams use proven frameworks and reusable components, reducing the time to develop an eWallet app and minimizing technical debt.

This approach helps startups test core features, gather user feedback, and refine functionality before scaling.

Example:

A startup testing a campus-based digital wallet outsourced development to quickly deploy limited features such as QR payments and transaction history.

User feedback guided eWallet app feature prioritization before full-scale investment.

As startups gain traction and begin scaling, a hybrid model often delivers the best results.

Outsourced teams handle development and scaling, while internal teams manage product strategy and user experience.

This balance ensures faster innovation without losing strategic control as the product and user base grow.

Example:

A growing US payment platform maintained an internal product team while outsourcing backend scaling.

This allowed faster feature releases without overloading internal resources.

VC-funded startups with strong financial backing may choose the right eWallet app developers for in-house development for long-term innovation.

Building an internal team enables deeper product customization, tighter integration with business goals, and stronger intellectual property ownership.

This model suits startups planning continuous feature expansion and long-term platform development.

Example:

After securing Series A funding, a fintech startup transitioned from outsourcing to an in-house team to build proprietary fraud detection and analytics capabilities.

For eWallet apps operating in highly regulated environments, outsourcing to fintech specialists significantly reduces compliance risks.

Experienced development partners understand US regulations such as PCI DSS, KYC, and AML, ensuring secure architecture, proper data handling, and smoother regulatory audits throughout the development lifecycle.

Example:

A startup offering cross-border payments partnered with a fintech development firm experienced in compliance, avoiding costly regulatory rework during its first external audit.

Startups with a long-term vision involving multiple fintech products may initially outsource development and later transition in-house.

This phased approach allows startups to launch faster, learn from real users, and gradually build internal expertise while maintaining stability and control as the product ecosystem expands.

Example:

A digital banking startup outsourced its first wallet product, then built an in-house team to develop lending and rewards modules as the platform matured.

Techanic Infotech is a trusted eWallet app development company with proven experience delivering secure, scalable, and regulation-compliant eWallet solutions.

We help US startups transform ideas into market-ready digital wallets by offering end-to-end development services, from product strategy and UI/UX design to deployment and post-launch support.

Our team follows industry best practices for PCI DSS, KYC, and AML compliance, ensuring data security and regulatory readiness.

With agile development methodologies, transparent communication, and flexible engagement models, we enable faster launches and predictable costs.

Whether you need an MVP or an enterprise-grade eWallet platform, Techanic Infotech delivers technology you can trust.

Choosing between in-house and outsourced eWallet app development depends on a startup’s budget, timeline, technical expertise, and long-term vision.

For most US startups, outsourcing offers a faster, more cost-efficient, and lower-risk path to launching a compliant digital wallet.

In-house development becomes more practical as startups scale, secure funding, and require deeper control over product evolution.

A hybrid approach often provides the optimal balance, leveraging outsourced expertise while gradually building internal capabilities.

Regardless of the model, success depends on strong planning, regulatory compliance, and selecting the right development partner.

In-house development uses an internal team for full control and IP ownership, while outsourcing relies on external fintech specialists for cost efficiency, faster time-to-market, and scalability.

Costs vary from $20,000 to $120,000. Outsourced MVPs typically range from $20,000 to $70,000, while in-house development ranges from $60,000 to $120,000, depending on features, compliance needs, and app complexity.

Outsourcing is ideal for early-stage startups, enabling quick MVP launches, reduced financial risk, and access to fintech expertise without the burden of hiring a full internal team.

Startups should partner with experienced fintech developers familiar with PCI DSS, KYC, and AML standards. Clear contracts, audits, and data protection agreements ensure regulatory compliance.

Startups may transition in-house once they secure funding, plan long-term product expansion, and need greater control over IP, security, and proprietary features for scalability and innovation.

Abhishek Jangid is the CEO of Techanic Infotech, with extensive experience in mobile app and web development. He specializes in helping businesses turn innovative ideas into scalable digital solutions through strategic planning and modern technology.