Key Takeaways

BNPL app development costs in 2026 range from $8,000 to $70,000+, depending on features, compliance requirements, app complexity, and the development team’s location and expertise.

A basic MVP helps businesses validate ideas quickly with minimal investment, while mid-level and enterprise apps offer advanced features, scalability, security, and better user experience.

Key cost-driving features include AI-based credit scoring, fraud detection systems, blockchain integration, multi-currency support, and advanced analytics dashboards for real-time insights and decision-making.

A robust technology stack with secure backend systems, scalable cloud infrastructure, reliable databases, and seamless payment gateway integration is essential for building a successful BNPL platform.

Regulatory compliance, including KYC, AML, PCI-DSS, and data protection laws, significantly impacts development cost but is critical for legal operation and user trust.

Businesses can reduce development costs by starting with an MVP, using third-party APIs, adopting agile methodologies, choosing the right development partner, and planning compliance early.

The Buy Now, Pay Later (BNPL) market continues to grow rapidly in 2026, driven by increasing digital payments, flexible credit demand, and eCommerce expansion.

In 2026, the cost to build a BNPL app typically ranges between $8,000 and $70,000+, depending on features, complexity, region, and compliance requirements.

From MVP development to enterprise-grade solutions with AI-based credit scoring and fraud detection, the overall investment varies significantly.

This guide breaks down everything you need to know about BNPL app development costs, features, and technology.

A Buy Now, Pay Later (BNPL) app lets customers purchase products instantly and split payments into smaller installments over time.

It partners with retailers, performs quick approvals, and manages scheduled repayments digitally.

As part of regulatory compliance, the platform conducts Know Your Customer (KYC) verification by validating identity documents through trusted third-party APIs.

Transactions are enabled only after successful identity or biometric authentication in eWallet apps, ensuring adherence to financial regulations and fraud prevention standards.

The platform leverages advanced AI-driven credit assessment models to evaluate user creditworthiness.

By analyzing behavioral data, transaction history, alternative data sources, and soft credit checks, the system performs real-time risk profiling.

At checkout, customers select the Buy Now, Pay Later (BNPL) option and choose their preferred repayment schedule, such as bi-weekly or monthly installments.

The application transparently presents payment breakdowns, due dates, applicable fees, and total repayment amounts, empowering users to make informed financial decisions.

Upon transaction confirmation, the BNPL provider disburses the full purchase amount to the merchant, minus a pre-agreed service fee.

This ensures merchants receive immediate payment while transferring credit and collection risk to the BNPL platform.

Repayments are automatically deducted from the user’s linked bank account or card on scheduled due dates through a secure auto-debit system.

Proactive reminders and real-time notifications are sent prior to each installment to minimize missed payments and enhance repayment performance.

In the event of missed payments, the system applies predefined penalties, interest charges, or grace period policies as outlined in the agreement.

Advanced risk monitoring tools continuously analyze repayment behavior, dynamically adjust credit limits, and implement preventive controls to mitigate financial exposure and reduce default rates.

Advanced mobile app features significantly increase BNPL app development costs, especially when integrating complex credit risk assessment algorithms, AI-based fraud detection, and real-time payment processing systems.

Additionally, regulatory compliance tools, multi-currency support, blockchain integration, and strong data security infrastructure require extra development time, expertise, and investment.

Leverages advanced machine learning algorithms to evaluate behavioral patterns, transactional histories, alternative credit data, and real-time financial signals.

While significantly improving credit scoring accuracy and decision automation, it demands complex data engineering, model training, and regulatory validation.

Deploys sophisticated real-time monitoring systems, behavioral biometrics, device fingerprinting, and AI-driven anomaly detection to identify suspicious activities instantly.

Building such systems requires complex rule engines, adaptive machine learning models, secure authentication layers, and continuous updates to counter evolving fraud tactics.

Utilizes distributed ledger technology to create immutable, tamper-resistant transaction records that enhance transparency, auditability, and trust.

However, implementation involves smart contract development, consensus mechanism configuration, scalability optimization, and cybersecurity hardening.

Enables dynamic currency conversion, cross-border payment processing, automated tax calculations, and adherence to international financial regulations.

Development complexity increases due to fluctuating exchange rates, regional compliance requirements, localization standards, reporting obligations, and integration with global banking networks.

Provides interactive dashboards, predictive analytics, mobile app development trends forecasting, and customizable financial reports to support strategic decision-making.

Implementation requires advanced data warehousing, ETL pipelines, visualization frameworks, role-based access controls, and high-performance processing capabilities for large-scale transactional datasets.

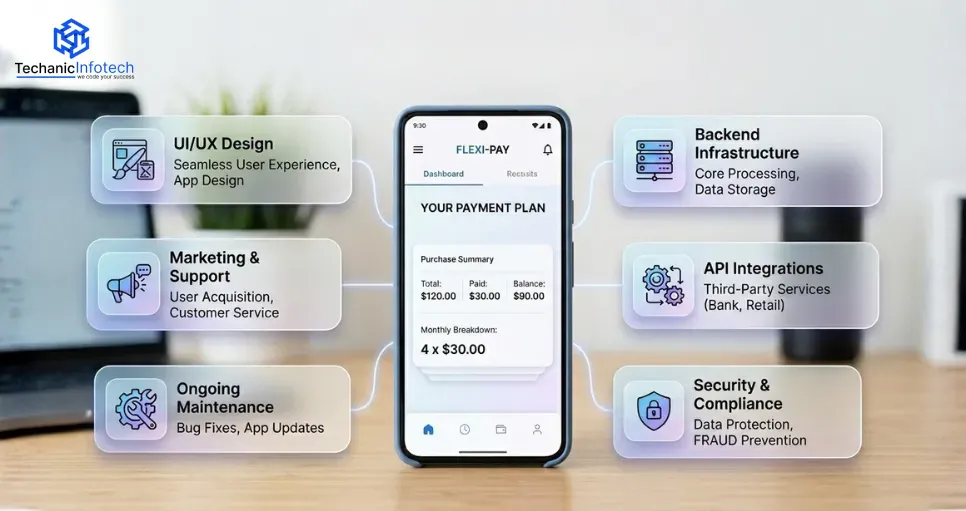

BNPL app development costs vary based on features, complexity, and technology requirements.

Key cost components include UI/UX design, frontend and backend development, payment gateway integration, security and compliance setup, testing, third-party APIs, and ongoing mobile app maintenance and updates.

A Basic MVP (Minimum Viable Product), priced between $8,000 and $15,000, focuses on delivering essential features required to validate your business idea in the market.

It includes core functionality, a clean but simple user interface, basic backend development, and limited integrations. Ideal for startups seeking fast deployment and early user feedback.

|

Feature Area |

Description |

Price Allocation (Approx.) |

|

Core Functionality |

Essential features to validate a business idea |

$2,000 – $3,000 |

|

Simple UI Design |

Clean, basic, and user-friendly interface |

$1,000 – $2,000 |

|

Basic Backend Development |

Server, database, and logic setup |

$1,500 – $3,000 |

|

Limited Integrations |

Basic third-party integrations (if needed) |

$2,000 – $3,500 |

|

Testing & Deployment |

QA testing and launch support |

$900 – $1,000 |

A Mid-Level App typically costs $15,000 to $30,000 and offers enhanced functionality, improved UI/UX design, third-party integrations, secure payment gateways, user authentication systems, and analytics tools.

Built with scalable architecture, it supports growing user traffic while delivering improved performance, security, reliability, and a more engaging overall user experience.

|

Feature Area |

Description |

Price Allocation (Approx.) |

|

Advanced Features |

Extended functionality beyond MVP |

$10,000 – $12,000 |

|

Enhanced UI/UX |

Professional, engaging interface design |

$6,000 – $8,000 |

|

Third-Party Integrations |

Payment gateways, APIs, and authentication systems |

$5,000 – $9,000 |

|

Scalable Architecture |

Performance optimization & infrastructure setup |

$5,000 – $12,000 |

|

Analytics & Security |

Tracking tools, data protection, and reliability |

$4,000 – $8,000 |

An Enterprise Solution ranges from $30,000 to $70,000+ and is engineered for large-scale operations, complex workflows, and high-volume user environments.

It features advanced security protocols, cloud-based infrastructure, API integrations, automation systems, custom dashboards, and compliance implementation.

Dedicated technical support, ensuring maximum scalability, operational efficiency, and long-term business sustainability.

|

Feature Area |

Description |

Price Allocation (Approx.) |

|

Cloud Infrastructure |

High-volume cloud-based system setup |

$5,000 – $10,000 |

|

Advanced Security |

Encryption, compliance frameworks |

$10,000 – $12,000 |

|

Custom API Integrations |

Complex system integrations & automation |

$12,000 – $14,000 |

|

Custom Dashboards |

Business intelligence & reporting tools |

$8,000 – $10,000 |

|

Dedicated Support & Optimization |

Ongoing scalability & performance tuning |

$10,000 – $15,000 |

Compliance and Licensing costs fall between $10,000 and $15,000, depending on industry and regional regulations.

This includes legal consultations, regulatory approvals, certifications, data protection compliance (such as GDPR or HIPAA), security audits, and mandatory licensing fees.

These investments ensure your application meets strict legal standards before public release.

|

Feature Area |

Description |

Price Allocation (Approx.) |

|

Legal Consultation |

Industry-specific legal advisory |

$2,500 – $8,000 |

|

Regulatory Approvals |

Certifications and approvals |

$2,000 – $6,000 |

|

Data Protection Compliance |

GDPR, HIPAA, regional compliance |

$3,000 – $7,000 |

|

Security Audits |

Risk assessment & vulnerability testing |

$4,000 – $8,000 |

|

Licensing Fees |

Government & industry licenses |

$1,000 – $3,000 |

Annual maintenance typically represents 15–20% of the total development cost per year. For example, a $70,000 application may require $9,000–$12,000 annually.

This covers ongoing bug fixes, security updates, server management, performance optimization, feature upgrades, compatibility updates, and continuous technical support to ensure stability and growth.

|

Feature Area |

Description |

Price Allocation (Approx.) |

|

Bug Fixes |

Ongoing issue resolution |

$2,000 – $4,000 |

|

Security Updates |

Regular patches & monitoring |

$2,500 – $3,000 |

|

Server Management |

Hosting & performance optimization |

$1,000 – $2,500 |

|

Feature Upgrades |

Enhancements & improvements |

$1,500 – $2,500 |

|

Technical Support |

Continuous assistance |

$1,500 – $2,500 |

Several factors influence BNPL app development costs, including app complexity, feature set, and level of customization required.

Other key factors include technology stack selection, security and compliance requirements, third-party integrations, an eWallet app development company location, testing processes, and ongoing maintenance and support needs.

App complexity significantly impacts development cost. A simple BNPL app with basic checkout financing costs less than one featuring AI-based credit scoring.

Real-time analytics, multi-merchant integration, dashboards, dispute management, and automated repayment systems.

BNPL apps must comply with financial regulations, consumer protection laws, and lending guidelines that vary by region.

Meeting licensing, KYC, AML, and financial reporting standards increases legal, documentation, and audit expenses.

Adhering to security standards like PCI-DSS and GDPR increases development costs due to encryption protocols, secure APIs, tokenization, fraud detection systems, and regular security audits.

Protecting financial and personal data requires advanced cybersecurity infrastructure, penetration testing, and compliance monitoring to prevent breaches and legal penalties.

Teams in North America or Western Europe typically charge higher hourly rates compared to Asia or Eastern Europe.

However, pricing differences also reflect expertise, communication efficiency, project management standards, and overall delivery quality.

Ongoing maintenance affects long-term costs. BNPL apps require continuous monitoring, bug fixes, server optimization, security patches, compliance updates, and feature enhancements.

As regulations evolve and user demand grows, regular upgrades and performance improvements become essential to maintain competitiveness and system reliability.

Reducing BNPL app development costs starts with building a clear MVP that includes only essential features like user registration, payment scheduling, and basic credit checks.

Additionally, using cross-platform frameworks, reliable third-party APIs, and cloud infrastructure can significantly shorten development time and lower expenses.

Begin with a Minimum Viable Product focusing only on essential BNPL features like user registration, checkout financing, repayment tracking, and basic admin controls.

Launching a lean version reduces upfront costs, speeds market entry, and allows real-user feedback before investing in advanced functionality.

Instead of building everything from scratch, integrate reliable third-party payment gateways, identity verification tools, credit scoring APIs, and cloud services.

Leveraging pre-built solutions significantly lowers development time, reduces engineering complexity, and ensures tested reliability with lower infrastructure expenses.

Skilled teams follow optimized workflows, reusable frameworks, and efficient coding standards.

This minimizes rework, shortens time to develop an eWallet app, ensures regulatory alignment, and improves overall cost-efficiency throughout the project lifecycle.

Agile methodology allows phased releases, iterative testing, and continuous improvement. By prioritizing features strategically, businesses avoid unnecessary development expenses.

Agile also helps identify risks early, reduce scope creep, and maintain better budget control during the entire development process.

Address regulatory and security requirements at the planning stage rather than later. Early compliance integration prevents expensive redesigns, penalties, and delays.

Proactive legal consultation and structured documentation streamline approval processes while reducing long-term compliance management costs.

Buy Now, Pay Later (BNPL) applications come in various models based on how payments are structured and who provides the financing.

Common types include short-term installment apps, long-term financing platforms, and retailer-specific BNPL solutions tailored to different consumer needs.

These standalone Buy Now, Pay Later (BNPL) applications are designed specifically for end consumers, enabling them to shop across a wide network of online and offline merchants.

They offer flexible repayment structures, personalized spending limits, real-time credit tracking dashboards, and transaction insights.

Merchant-integrated BNPL solutions are embedded directly into eCommerce websites, mobile apps, or point-of-sale (POS) systems.

This seamless integration ensures a frictionless checkout experience, allowing customers to select installment payment options without being redirected to external platforms.

White-label BNPL platforms provide ready-to-deploy infrastructure that enables financial institutions, fintech startups, or retailers to launch their own branded BNPL services.

These turnkey solutions significantly reduce development time, operational complexity, and upfront eWallet app development cost.

Traditional banks are increasingly incorporating BNPL features within their existing mobile banking ecosystems.

By leveraging established customer relationships, transaction history, and regulatory infrastructure, banks can offer pre-approved installment plans with enhanced eWallet app security and compliance oversight.

B2B-focused BNPL platforms cater to business transactions, enabling companies to purchase inventory, raw materials, equipment, or services with structured repayment terms.

These solutions improve working capital management, enhance cash flow flexibility, and support supply chain efficiency.

Cross-border BNPL platforms facilitate international transactions by supporting multi-currency payments and global merchant networks.

They require sophisticated compliance management, currency conversion capabilities, cross-border payment gateways, and adherence to diverse regulatory environments.

Building a BNPL app requires a scalable mobile app tech stack, including frontend frameworks like React Native or Flutter and backend technologies such as Node.js or Django.

It also needs secure payment gateways, cloud hosting, databases, and strong data encryption for safe transactions.

Modern cross-platform frameworks such as React Native and Flutter enable rapid development of high-performance mobile applications with a unified codebase.

They ensure consistent UI/UX across Android and iOS, support real-time updates, enable responsive design systems, and integrate smoothly with backend APIs and third-party services.

Robust backend technologies like Node.js, Python, or Java power server-side logic, installment calculations, transaction processing, user authentication, and credit risk evaluation algorithms.

These frameworks support scalable microservices architectures, secure API development, asynchronous processing, and seamless integration with financial institutions and payment networks.

Reliable database systems such as PostgreSQL and MongoDB securely manage user profiles, transaction histories, repayment schedules, and audit logs.

They provide data consistency, high availability, encryption capabilities, backup mechanisms, indexing optimization, and support for handling large volumes of structured and unstructured financial data.

Cloud platforms like AWS, Microsoft Azure, and Google Cloud deliver scalable computing resources, secure storage, automated deployment pipelines, and global content delivery.

They enable high availability, disaster recovery planning, compliance support, monitoring tools, and mobile app development cost optimization for growing BNPL applications.

Integrating trusted payment gateways such as Stripe, PayPal, and Razorpay ensures secure transaction processing, tokenized payments, fraud screening, and global currency support.

Implementation requires API configuration, webhook management, reconciliation systems, compliance adherence, and seamless checkout experiences for merchants and customers.

Advanced security measures, including SSL encryption, biometric authentication, tokenization, and multi-factor authentication, protect sensitive financial data.

Development involves implementing secure coding standards, penetration testing, data masking, compliance audits, and intrusion detection systems.

Developing a BNPL app requires careful planning, regulatory awareness, and strong technical execution.

Costs vary depending on complexity, compliance requirements, security standards, and development expertise.

While initial investment may seem significant, a well-built BNPL platform offers substantial revenue opportunities in today’s rapidly growing digital payment ecosystem.

Businesses should focus on launching a streamlined MVP first, then gradually expand features based on market demand.

BNPL app development typically ranges from $8,000 to $70,000+, depending on complexity, compliance requirements, features, integrations, and security standards.

Developing a BNPL app usually takes 3 to 9 months. Timeline depends on app complexity, feature set, regulatory approvals, testing phases, and development team expertise.

Yes, BNPL apps must comply with financial regulations, KYC, AML laws, and data protection standards. Non-compliance can result in heavy penalties, legal action, and reputational damage.

BNPL apps commonly use secure cloud infrastructure, payment gateway integrations, AI-based credit scoring systems, encrypted databases, and scalable backend frameworks such as Node.js, Python, or Java.

BNPL apps generate revenue through merchant fees, interest charges, late payment fees, subscription models, and partnerships with financial institutions. A diversified monetization strategy improves long-term profitability.

A BNPL MVP should include core features such as user registration, KYC verification, basic credit assessment, checkout financing, repayment scheduling, and an admin dashboard.

They require lower upfront investment, faster deployment, and allow businesses to test the market before scaling into more complex models like B2B or cross-border BNPL platforms.

AI significantly increases development costs due to the need for data modeling, machine learning algorithms, and real-time processing.

Cloud infrastructure ensures scalability, data security, and high availability by allowing BNPL apps to handle large transaction volumes, enabling faster deployment.

Yes, BNPL apps can support international transactions through multi-currency integration and global payment gateways.

Abhishek Jangid is the CEO of Techanic Infotech, with extensive experience in mobile app and web development. He specializes in helping businesses turn innovative ideas into scalable digital solutions through strategic planning and modern technology.