The rapid growth of Buy Now, Pay Later (BNPL) services has transformed how consumers shop online, making Klarna one of the most influential fintech platforms globally.

Developing a Klarna clone app allows businesses to tap into this high-demand market by offering flexible, interest-free installment payments.

A BNPL app bridges the gap between merchants and customers, increasing conversion rates, average order values, and customer loyalty.

However, building such an app requires careful planning, regulatory compliance, secure payment systems, and scalable technology.

From credit risk assessment to seamless checkout experiences, every component must be optimized for trust and performance.

This guide explains the market opportunities, features, technology stack, development process, costs, and challenges involved in building a Klarna-like BNPL application.

Revenue for the Klarna app reached a record $903 million, reflecting exceptional momentum with +26% LfL growth and +28% reported growth.

Gross Merchandise Value (GMV) climbed to $32.7 billion, driven by sustained demand and platform expansion, delivering +23% LfL growth and a standout +43% increase in the U.S., highlighting accelerating regional performance.

The Klarna Card recorded 4 million signups since July, rapidly scaling adoption and now accounting for 15% of global transactions in October.

User and merchant growth reached new highs, with 27 million new users and a record 235,000 new merchants onboarded.

Fair Financing U.S. GMV surged 244%, demonstrating exceptional traction, strong consumer uptake, and significant gains in market share in a highly competitive landscape.

By the end of 2026, Klarna aims to add 35.2 million new users, growing at an average annual rate of 38.2%.

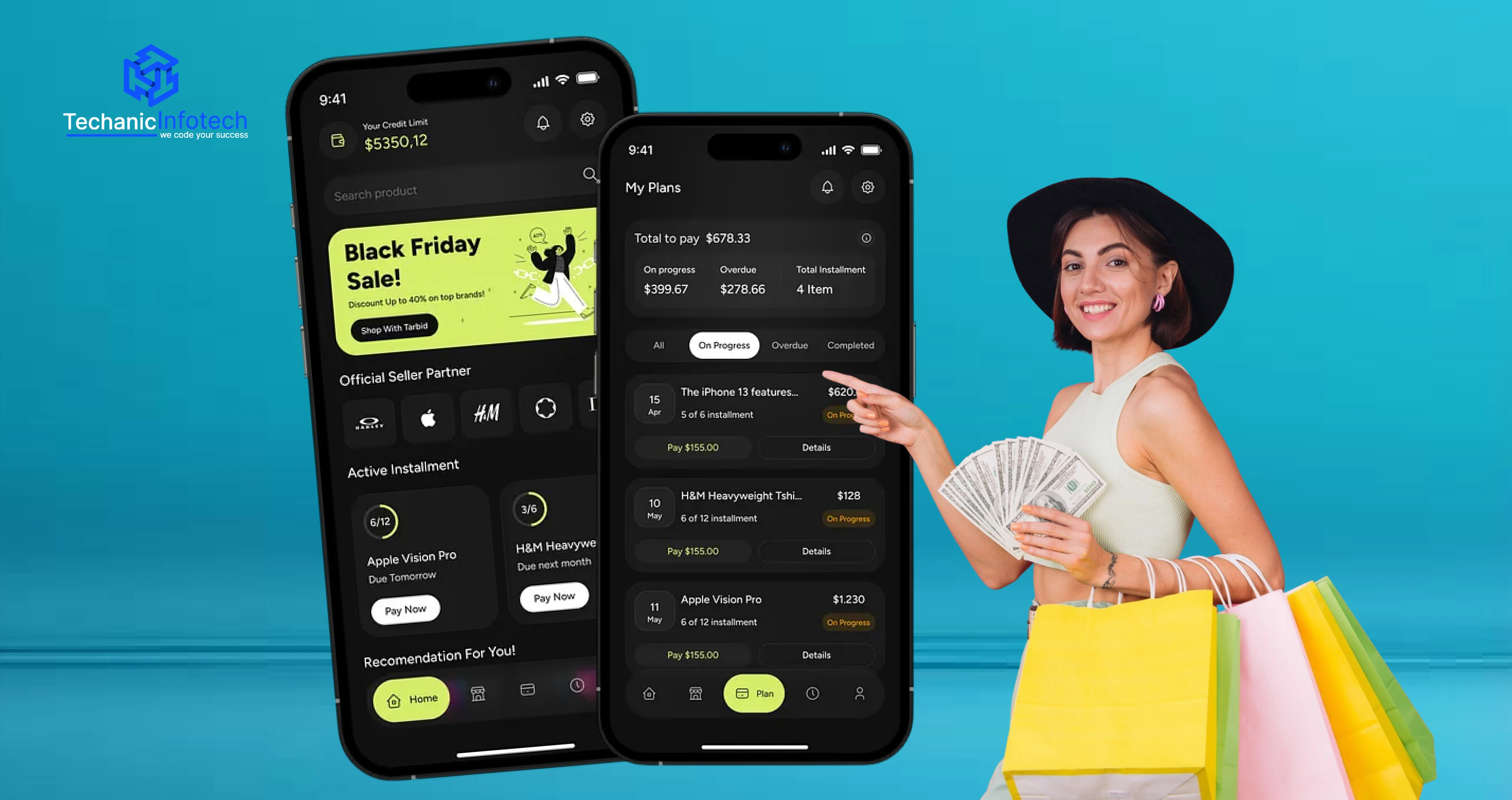

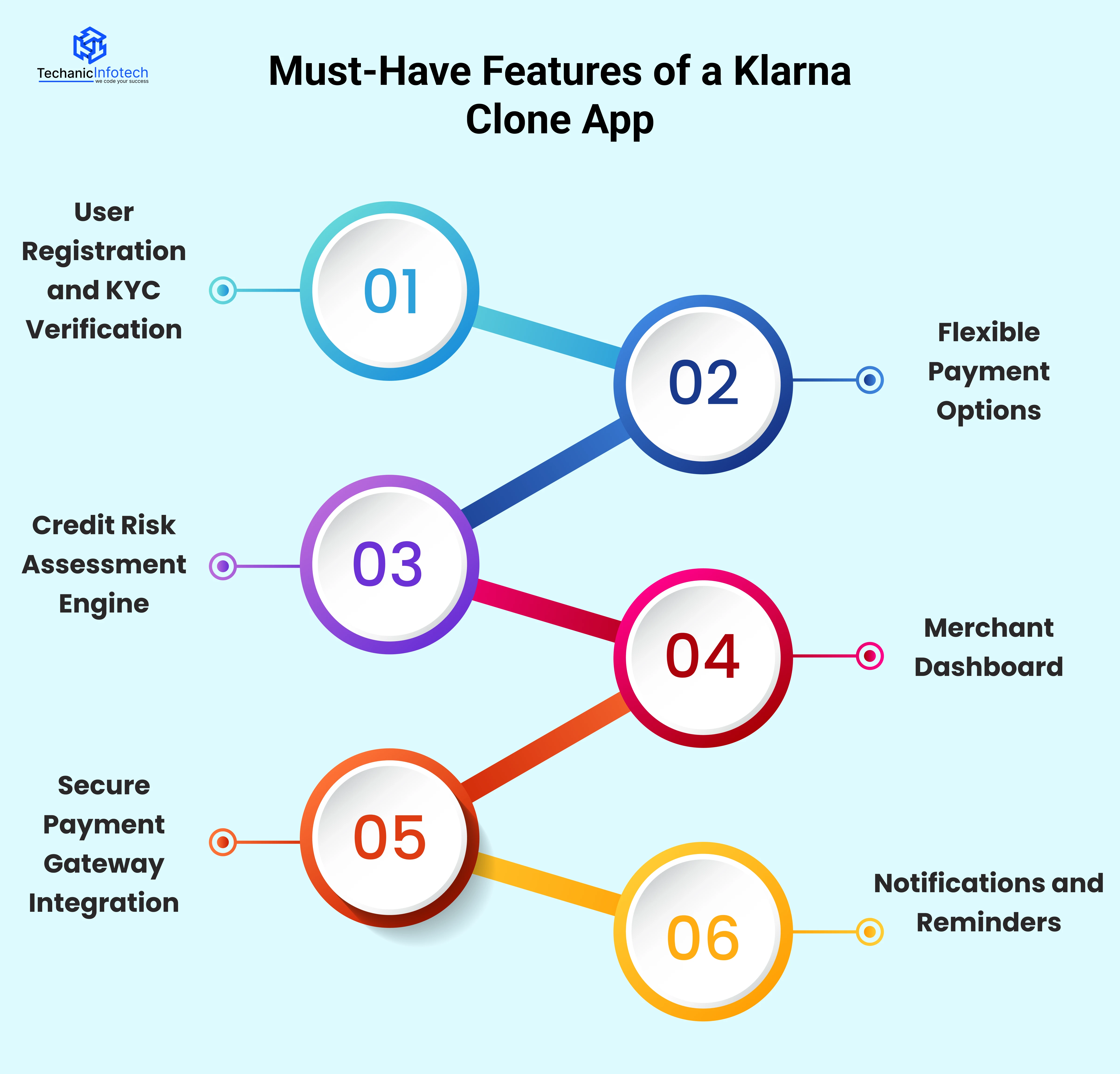

A Klarna clone app must offer seamless checkout, flexible installment plans, instant credit decisions, secure payment processing, fraud prevention, and easy merchant integrations.

The following are the list of the top eWallet app features that must be in the Klarne clone application.

A secure and streamlined onboarding process enables users to register quickly via mobile number or email while completing KYC verification through government-approved documents.

Not only this, but it also includes real-time identity validation systems, ensuring regulatory compliance, fraud prevention, and long-term platform trust.

The platform offers multiple BNPL repayment models, including pay-in-4, monthly installments, and deferred payments.

These flexible options increase user adoption while allowing merchants to tailor payment plans based on transaction value, customer behavior, and calculated risk profiles.

An advanced AI-driven credit risk engine evaluates user data, repayment history, behavioral patterns, and transaction insights in real time.

This enables instant approval or rejection decisions, reduces default rates, and safeguards profitability while maintaining a frictionless checkout experience.

A robust merchant dashboard provides real-time visibility into sales performance, settlements, refunds, and customer behavior.

Actionable analytics empower merchants to monitor BNPL performance, improve checkout conversion rates, and make data-driven business decisions with confidence.

Seamless integration with trusted payment gateways ensures fast and reliable fund transfers.

Enterprise-grade eWallet app security measures, including encryption, tokenization, and fraud detection systems, protect sensitive financial data and reinforce user and merchant trust at every transaction stage.

Automated payment reminders delivered through push notifications, SMS, and email keep users informed about upcoming dues.

Timely communication reduces missed payments, improves repayment rates, and enhances user satisfaction while supporting responsible credit usage.

To build a Klarna-like BNPL app, you need a robust, scalable, and secure technology stack that supports real-time payments, credit decisions, and high availability.

Following are the clean breakdown of the eWallet app tech stack that was included in developing the Klarne clone:

Technologies like React.js, Next.js, Flutter, or React Native are used to build fast, responsive, and user-friendly interfaces.

These frameworks ensure smooth checkout flows, installment displays, and cross-platform consistency across web and mobile devices.

Node.js, Django, or Spring Boot power the backend to manage business logic, user accounts, installment plans, and payment workflows.

A scalable backend ensures high availability, fast API responses, and seamless merchant-consumer interactions.

PostgreSQL, MySQL, or MongoDB store transactional data, repayment schedules, user profiles, and merchant records.

A robust database architecture ensures data accuracy, quick retrieval, and compliance with financial data integrity standards.

eWallet API integration with Stripe, Adyen, PayPal, or banking APIs enables secure payment processing, refunds, and settlements.

These APIs support installment payments, fraud checks, and real-time transaction validation essential for BNPL platforms.

Technologies like OAuth 2.0, JWT, SSL encryption, and PCI-DSS compliance tools protect sensitive financial data.

Security layers prevent fraud, ensure user trust, and meet regulatory requirements in fintech and digital lending ecosystems.

AWS, Google Cloud, or Azure provide scalable hosting, load balancing, and disaster recovery.

DevOps tools like Docker, Kubernetes, and CI/CD pipelines enable faster deployments, reliability, and cost-efficient infrastructure management.

Building a Klarna-style Buy Now, Pay Later (BNPL) app requires a structured, compliance-first eWallet app development approach that balances seamless user experience, secure financial operations, and scalable technology.

The following step-by-step process outlines how to transform the eWallet app ideas into a market-ready solution.

This phase defines target users, regions, regulations, and core BNPL features.

Competitive analysis helps identify differentiators, while technical requirements ensure the product aligns with financial laws, user expectations, and scalability goals.

Mobile app design intuitive interfaces for shoppers and merchants, focusing on clarity during checkout and repayment.

Wireframes and prototypes ensure frictionless navigation, trust-building visuals, and high conversion rates across devices.

Develop secure APIs to handle user authentication, payment scheduling, merchant onboarding, and transaction processing.

This step establishes the core logic that powers installment calculations, approvals, and real-time payment status updates.

Integrate payment gateways, credit checks, and risk assessment engines.

Automated decision-making ensures instant approvals or rejections while minimizing default risks and maintaining compliance with regional lending regulations.

Conduct functional, performance, and security testing to identify vulnerabilities and bugs.

Compliance testing ensures adherence to PCI-DSS and data protection laws, delivering a stable, secure, and trustworthy BNPL application.

Deploy the application on cloud infrastructure and publish an app on App Store.

Proper monitoring, analytics, and logging tools ensure smooth launch, uptime stability, and early issue detection.

Ongoing updates improve performance, add new features, and adapt to regulatory changes.

Continuous optimization ensures scalability, better user experience, and long-term competitiveness in the evolving fintech market.

The cost to develop a Klarna clone app depends on multiple factors, including feature complexity, platform selection, security requirements, and regulatory compliance.

Below is a detailed breakdown of the key eWallet app development cost components involved in building a scalable and secure Buy Now, Pay Later solution.

A basic Klarna-like BNPL app within the $10,000–$30,000 range includes essential features such as user onboarding, installment payments, and basic merchant checkout.

It is ideal for startups looking to validate their concept with limited integrations before expanding features, markets, and regulatory coverage.

This table covers the core functionality of the BNPL app, ensuring users can sign up, make installment payments, and complete merchant transactions seamlessly.

UI/UX design typically costs $5,000–$15,000, covering custom interfaces, branding, wireframes, prototypes, and usability testing.

A polished, intuitive design enhances user trust, engagement, and conversion rates, which is especially critical for fintech applications handling payments and consumer credit.

Backend development and payment integration usually range from $3000–$10,000, including server architecture, payment gateways, installment logic, APIs, and transaction processing.

Costs increase with real-time payments, complex credit rules, scalability requirements, and multiple merchant or banking integrations.

Security and compliance implementation costs $5000–$10,000, covering PCI-DSS compliance, encryption, fraud prevention, secure authentication, and regulatory requirements such as KYC and AML.

These investments are essential to safeguard financial data and ensure legal operation across different regions.

Testing, deployment, and maintenance typically cost $4000–$7000, including quality assurance, security testing, cloud deployment, monitoring, and initial support.

Ongoing maintenance ensures system stability, performance optimization, scalability, and continued compliance after product launch.

Following is the table that shows the complete price estimate as per the steps or feature area in the Klarna clone app.

|

Component / Feature Area |

Pricing Range (USD) |

Key Features Included |

Complexity Level |

|

App Complexity & Core Feature Set (BNPL MVP) |

$10,000 – $30,000 |

• User onboarding & account setup • Installment payment functionality • Basic merchant checkout • Core BNPL transaction flow • Startup-ready architecture |

Low–Medium |

|

UI/UX Design Costs |

$5,000 – $15,000 |

• Custom UI components • Branding & visual identity • Wireframes & prototypes • Usability & UX testing • Conversion-focused design |

Medium |

|

Backend & Payment Integration |

$3000 – $10,000 |

• Backend server architecture • Payment gateway integration • Installment logic & APIs • Transaction processing • Merchant & banking integrations |

High |

|

Security & Compliance Implementation |

$5000 – $10,000 |

• PCI-DSS compliance • Data encryption & secure storage • Fraud detection & prevention • KYC & AML implementation • Regulatory compliance support |

High |

|

Testing, Deployment & Maintenance |

$4000 – $7000 |

• Functional & security testing • Cloud deployment & monitoring • Performance optimization • Initial post-launch support • Scalability & compliance checks |

Medium |

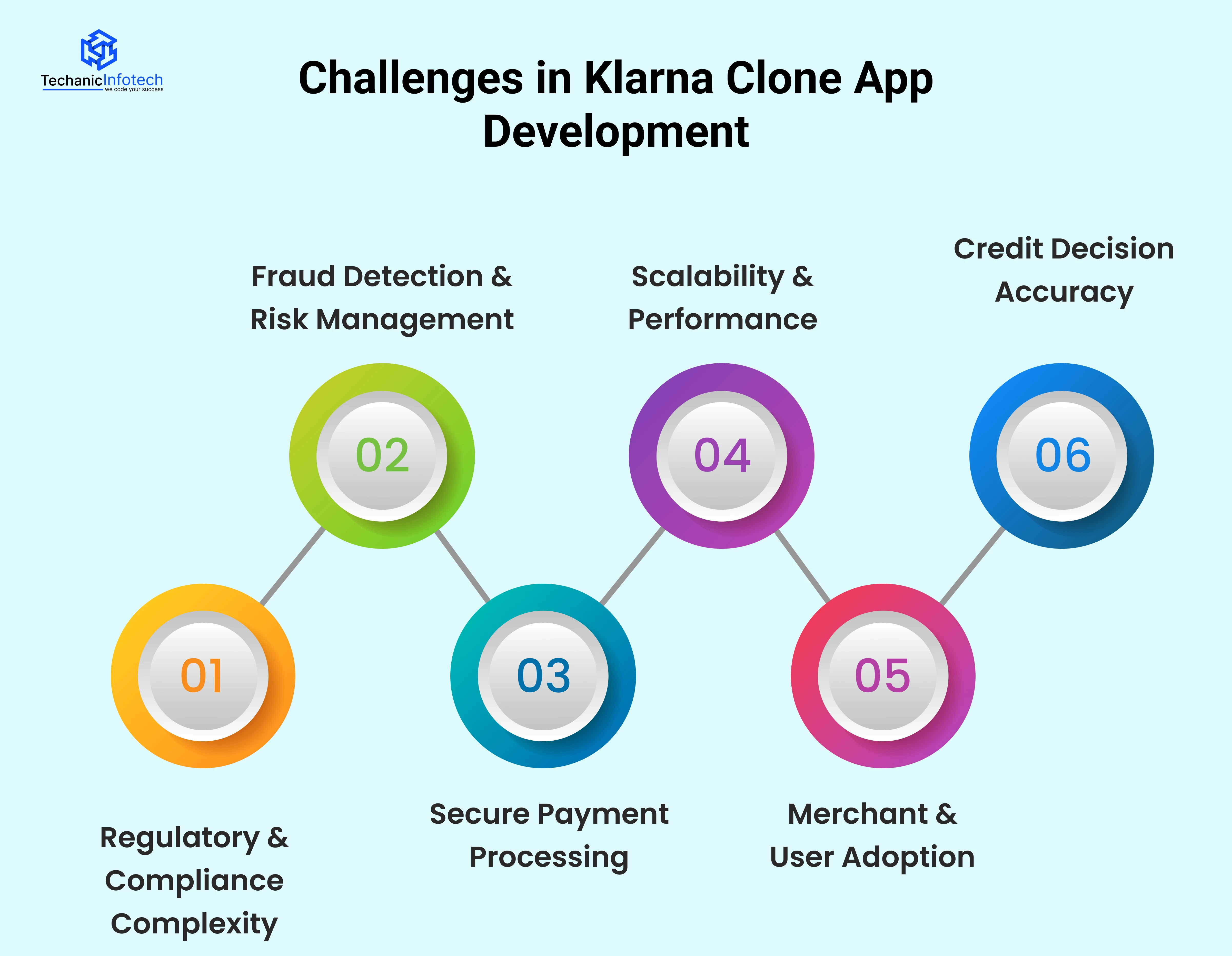

Developing a Klarna clone app comes with several unique challenges, ranging from regulatory compliance to ensuring seamless user experience and secure transactions.

Below is a detailed overview of the key technical, operational, and market-related challenges faced during development.

BNPL platforms must navigate complex and evolving financial regulations, lending laws, and data protection requirements across multiple jurisdictions.

Staying compliant demands legal expertise, constant monitoring of regulatory changes, and robust internal governance frameworks to avoid penalties and operational risk.

BNPL services face heightened exposure to fraud, identity theft, and payment defaults.

Implementing advanced risk engines, real-time transaction monitoring, and machine-learning-driven fraud detection is essential to protect the platform.

It's also helpful in maintaining a seamless, low-friction user experience.

Processing large volumes of financial transactions requires enterprise-grade security.

Ensuring PCI-DSS compliance, strong encryption, tokenization, and secure API integrations is technically demanding.

Not only this, but it's also critical to safeguarding sensitive data, preventing breaches, and maintaining long-term user and merchant trust.

As user and merchant adoption accelerates, BNPL platforms must handle surging transaction volumes and peak usage periods.

Building a highly scalable, resilient architecture with real-time processing, low latency, and minimal downtime presents significant engineering and infrastructure challenges.

Attracting merchants and users to a new BNPL solution requires intuitive UX, transparent pricing, and clear repayment terms.

Establishing credibility in a crowded fintech landscape demands strategic partnerships, strong branding, and consistent delivery of value and reliability over time.

Delivering instant approvals while practicing responsible lending is a delicate balance.

Inaccurate credit decisions can lead to higher default rates or lost customers, directly affecting profitability, regulatory scrutiny, and the long-term sustainability of the BNPL platform.

Techanic Infotech is a trusted eWallet app development company specializing in secure, scalable BNPL solutions.

With extensive experience in payment systems, credit risk engines, and regulatory compliance, Techanic Infotech delivers high-performance Klarna clone apps tailored to business needs.

Their expert team focuses on intuitive UI/UX, robust backend architecture, and seamless third-party integrations.

From ideation and development to deployment and post-launch support, they provide end-to-end services.

By leveraging modern technologies and agile methodologies, Techanic Infotech ensures faster time-to-market and cost-effective solutions.

Partnering with them helps businesses launch reliable BNPL platforms that drive growth, merchant adoption, and long-term customer trust.

Developing a Klarna clone app is a strategic move for businesses looking to capitalize on the booming BNPL market.

With rising consumer demand for flexible payments, such apps offer immense revenue and partnership opportunities.

However, success depends on robust technology, secure payment systems, accurate credit assessment, and regulatory compliance.

From market research and feature planning to development and maintenance, each step must be carefully executed.

While development costs range from $10,000 to $90,000+, the long-term returns justify the investment.

By partnering with an experienced fintech development company, businesses can launch scalable, secure, and user-friendly BNPL solutions that compete effectively in today’s digital finance ecosystem.

A Klarna clone app uses real-time data analysis, transaction behavior, AI-driven risk models, and alternative credit scoring to assess user eligibility instantly while minimizing defaults.

BNPL apps must comply with KYC, AML, PCI-DSS, GDPR, and country-specific financial regulations to ensure legal operation, secure transactions, and long-term user trust.

Yes, the app can be customized for retail, healthcare, travel, or education, with region-specific currencies, tax rules, repayment plans, and compliance requirements.

Revenue is generated through merchant commissions, late payment fees, premium merchant services, promotional placements, and strategic partnerships with banks and retailers.

Scalability depends on cloud infrastructure, backend architecture, database optimization, payment gateway reliability, and the ability to handle high transaction volumes securely.

Abhishek Jangid is the CEO of Techanic Infotech, with extensive experience in mobile app and web development. He specializes in helping businesses turn innovative ideas into scalable digital solutions through strategic planning and modern technology.